31

Oct

An example of the application of going concern concept of accounting is the computation of depreciation on the basis of expected economic life of fixed assets rather than their current market value. D applying the conservatism convention.

An example of an accounting assumption is. An example of an accounting assumption is a going concern. Accounting system statement and computerized accounting are not assumptions. See page 35 for more details.

An example of an accounting assumption is an. An accounting assumption is a set of rules that helps to ensure financial reports of the business are prepared in line with applicable accounting standards. It lays a strong foundation for consistent reliable objective and valuable financial information.

In a business it is the entrepreneur who ____. Service merchandising and manufacturing. The type of business that provides a product or a service makes sales to customers and incurs expenses is.

A business has the ability to operate indefintely. An example of an. Solved Example for You.

Are there any limitations to the accounting assumptions. Yes there are certain limitations to accounting assumptions and principles. For example Going Concern.

It assumes that an entity will continue indefinitely. Practically though this is hardly ever the case. Firm is an example of A following the going concern assumption.

B applying the realization principle. C following the separate entity assumption. D applying the conservatism convention.

Depreciating equipment over its useful life is an example of A following the objectivity assumption. B applying the matching principle. Essay Example on Assumption Principles And Constraints Of Accounting Economic entity assumption is the activities of the entity be kept separate and distinct from the activities of the owner and all other economic entities.

Another example of going concern is the writing off the deferred expense. The benefit of such expenses is enjoyed through different years instead of utilizing the expense in a single year. This is too conceivable because of going concern fundamental accounting assumption.

Transactions are recorded using the accrual basis of accounting where the recognition of revenues and expenses arises when earned or used respectively. If this assumption is not true a business should instead use the cash basis of accounting to develop financial statements that are based on cash flows. Assumptions can be predictions of the future such as probabilities or expert forecasts.

For example a ski hill that documents an assumption in a business plan that there will be at least 28 days of snow each season for the next 10 years based on climate predictions. As each assumption is discussed try to understand why it has evolved and be especially aware of those that fail to capture the world as it really is. The most fundamental assumption of financial accounting involves the object of the performance measure.

An assumption is something that you assume to be the case even without proof. For example people might make the assumption that youre a nerd if you wear glasses even though thats not true. Finally What are the underlying assumptions in the preparation of financial statements What are the Key Accounting Assumptions.

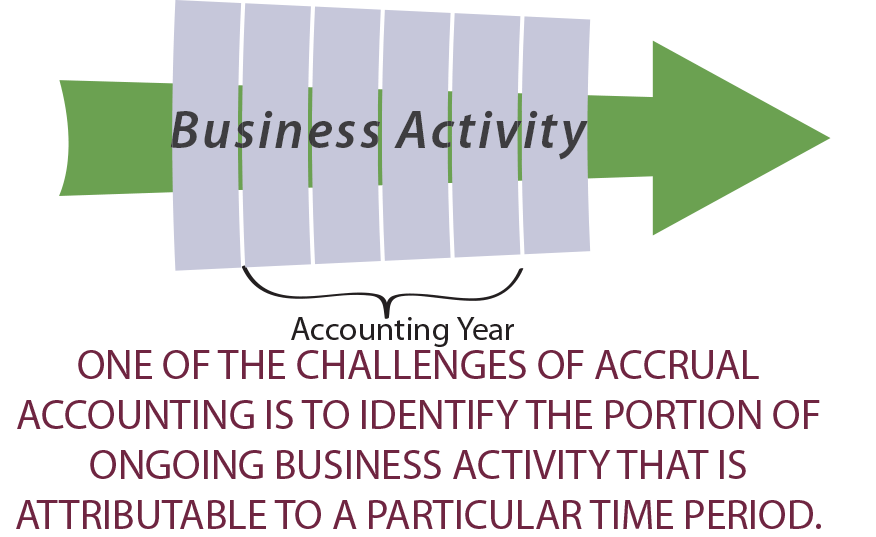

The accounting period assumption is needed to allow a companys financial health to be tracked over time in a way that allows fair comparisons. Exceptions If there is specific evidence that the business has closed or will imminently cease trading the. Example of Periodicity Assumption.

For example management is considering to invest the new projects which are similar to the existing one. In order to make the correct decision management needs to assess and predict the expected gain on the new investment. Note that an accounting period that is less than a year is known as an interim period while an accounting period of 12 months is known as the fiscal year.

However despite the simplicity of the accounting period assumption some transactions cannot be assigned to a particular accounting period easily Also see Cash vs Accrual Accounting Methods. An example of the application of going concern concept of accounting is the computation of depreciation on the basis of expected economic life of fixed assets rather than their current market value. Companies assume that their business will continue for an indefinite period of time and the assets will be used in the business until fully.

There are four assumptions such as continuity business entity money measurement and accounting period assumption.

Previous post

An introduction to database systems